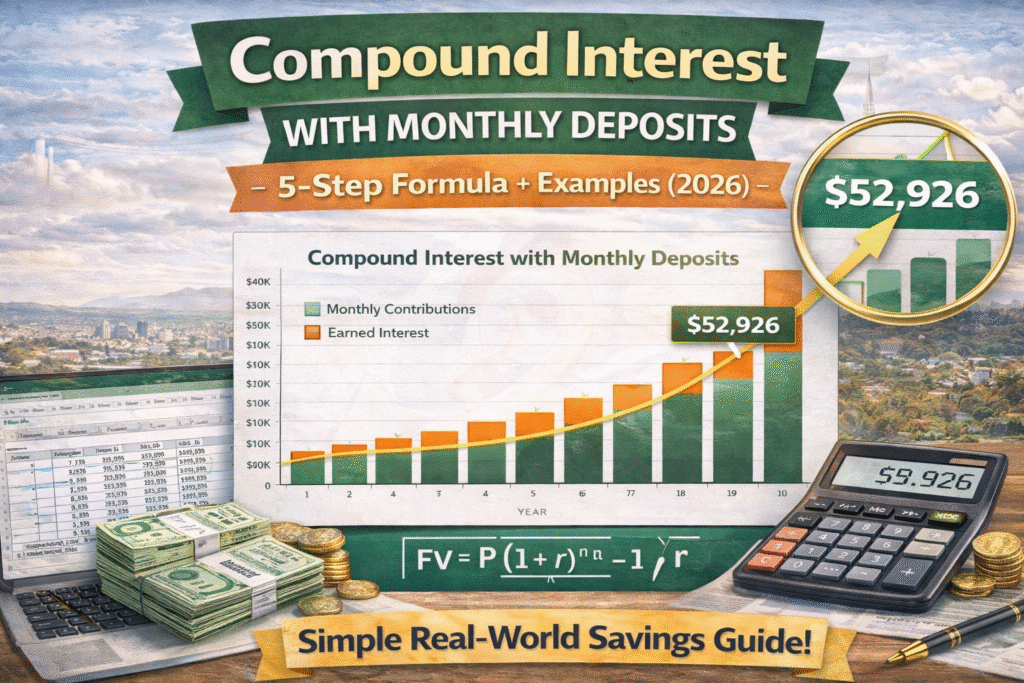

Compound Interest With Monthly Deposits: 5-Step Formula + Examples (2026)

Compound interest with monthly deposits is the fastest realistic way most people build long-term savings.

It combines two powerful forces:

your regular monthly contributions plus interest on your interest.

This step-by-step guide shows the exact formulas, calculator method, and simple examples you can copy into Excel.

External learning (dofollow):

Investor.gov Compound Interest Calculator |

SEC: Compounding explained

Internal links (replace with your pages):

Simple vs Compound Interest |

Budgeting Guide |

Best Investment Options

What is compound interest?

Compound interest means you earn interest on your original money (principal) and on the interest already earned.

Over time, this “interest on interest” creates accelerating growth.

If you invest for longer and contribute regularly, compounding becomes much stronger—this is why

compound interest with monthly deposits is so popular for savings and retirement goals.

Compound interest with monthly deposits (why it’s different)

The basic compound interest formula assumes a single lump sum. But in real life, many people deposit money every month.

That means:

- Your first deposit compounds for the longest time.

- Each later deposit compounds for fewer months.

- The total future value is the sum of a growing series (an annuity).

So the correct method for compound interest with monthly deposits is a

future value (FV) of an annuity calculation.

Compound interest formula (with monthly contributions)

1) Growth of your starting amount (lump sum)

FV (lump sum) = P × (1 + r)n

2) Growth of monthly deposits (ordinary annuity)

FV (deposits) = PMT × [((1 + r)n − 1) ÷ r]

3) Total future value

Total FV = P × (1 + r)n + PMT × [((1 + r)n − 1) ÷ r]

Meaning of the symbols

- P = starting principal (your initial amount)

- PMT = monthly deposit (your contribution each month)

- r = monthly interest rate (annual rate ÷ 12)

- n = total number of months (years × 12)

This is the core formula used in any proper

compound interest with monthly deposits calculator.

How to calculate compound interest with monthly deposits (5 steps)

- Write your inputs: starting amount (P), monthly deposit (PMT), annual interest rate, and total years.

- Convert annual rate to monthly rate:

r = (Annual Rate ÷ 100) ÷ 12

- Convert years to months:

n = Years × 12

- Calculate FV for the lump sum:

P × (1 + r)n

- Calculate FV for monthly deposits and add:

PMT × [((1 + r)n − 1) ÷ r]

Then add the lump sum FV + deposit FV.

If you deposit at the beginning of each month (not the end), multiply the deposit part by (1 + r)

because each deposit gets one extra month of growth.

Examples: compound interest with monthly deposits

Example 1 (most common): No initial amount, monthly deposit only

Suppose you deposit PKR 10,000 per month for 5 years at 12% per year compounded monthly.

- P = 0

- PMT = 10,000

- Monthly rate r = 12% ÷ 12 = 1% = 0.01

- n = 5 × 12 = 60

FV = 10,000 × [((1.01)60 − 1) ÷ 0.01]

≈ PKR 816,700 (rounded).

Total deposits = 10,000 × 60 = PKR 600,000 → growth gained ≈ PKR 216,700 due to compounding.

Example 2: Initial amount + monthly deposits

Start with PKR 200,000 and add PKR 15,000 per month for 10 years at 10% annual, monthly compounding.

- P = 200,000

- PMT = 15,000

- r = 10% ÷ 12 = 0.8333% = 0.008333

- n = 10 × 12 = 120

Total FV = P × (1 + r)n + PMT × [((1 + r)n − 1) ÷ r]

≈ PKR 3,680,000 (rounded).

These examples show why compound interest with monthly deposits becomes powerful over longer time periods.

Excel compound interest calculator (easy FV formulas)

Excel can calculate compound interest with monthly deposits instantly with the FV() function.

Excel FV formula (end-of-month deposits)

=FV((AnnualRate/12), Years*12, -MonthlyDeposit, -InitialAmount, 0)

Excel FV formula (beginning-of-month deposits)

=FV((AnnualRate/12), Years*12, -MonthlyDeposit, -InitialAmount, 1)

Simple sheet layout (copy-paste)

| Cell | Label | Value |

|---|---|---|

| A2 | Initial Amount (P) | B2 = 200000 |

| A3 | Monthly Deposit (PMT) | B3 = 15000 |

| A4 | Annual Interest Rate | B4 = 10% |

| A5 | Years | B5 = 10 |

| A7 | Future Value (FV) | B7 =FV((B4/12), B5*12, -B3, -B2, 0) |

Tip: If your B4 is written as 10 instead of 10%, use (B4/100)/12.

Common mistakes (monthly vs annual rates)

Is 1% per month the same as 12% per annum?

Not exactly. 1% per month compounded monthly becomes:

(1.01)12 − 1 ≈ 12.68% effective annual rate.

While 12% per annum compounded monthly usually means a monthly rate of 12% ÷ 12 = 1%,

but the effective yearly growth is about 12.68%. That’s why compounding details matter.

Other common issues

- Using years instead of months: always convert to n = years × 12 for monthly deposits.

- Wrong deposit timing: end-of-month vs beginning-of-month changes the result.

- Ignoring fees/taxes: real returns may be lower after charges.

People also ask (FAQ)

How to calculate compound interest for monthly deposit?

Use the annuity future value formula:

FV = PMT × [((1 + r)n − 1) ÷ r],

where r is monthly rate and n is months. If you also have a starting amount, add

P × (1 + r)n. This is the correct method for compound interest with monthly deposits.

Is 1% per month the same as 12% per annum?

Compounded monthly, 1% per month has an effective annual rate of about 12.68%. So it’s not exactly the same as “12% simple”.

Always check whether the rate is quoted as nominal annual or effective.

What is the 7 3 2 rule of compounding?

The “7-3-2 rule” is often described as a quick mental reminder:

higher returns + more time + consistent contributions lead to faster compounding.

Many people also use the Rule of 72 to estimate how long it takes money to double:

Years to double ≈ 72 ÷ annual rate (%).

(Example: at 12%, doubling time ≈ 72 ÷ 12 = 6 years.)

How to calculate compound interest step by step?

Convert annual rate to monthly, convert years to months, compute growth factor (1 + r)n,

calculate the lump sum FV (if any), calculate the deposit FV, and add them together.

That’s the full step-by-step process used in every compound interest with monthly deposits calculator.