Is the 2026 Housing Market Cooling? Why Your Down Payment Matters More Now

As we navigate through February 2026, many prospective homebuyers and investors are asking the same critical question: Is the 2026 housing market cooling? After years of volatility, record-high interest rates, and a “lock-in” effect that kept inventory at historic lows, the real estate landscape is finally showing signs of a “Great Reset.” However, this isn’t a market crash—it’s a complex rebalancing where your entry strategy, specifically your down payment, has become the ultimate leverage.

In this comprehensive guide, we analyze current economic data, regional trends, and financial strategies to help you decide if now is the right time to buy. Whether you are a first-time buyer or a seasoned investor, understanding these shifts is essential for long-term wealth building.

Table of Contents

- The State of the 2026 Housing Market: Rebalance or Crash?

- 5 Key Signs the 2026 Housing Market is Cooling

- Why Your Down Payment Matters More in a Cooling Market

- The GEO Shift: Cooling Hotspots vs. Resilient Zones

- The Math: Using a Mortgage Calculator for 2026 Planning

- Frequently Asked Questions (AEO Optimized)

The State of the 2026 Housing Market: Rebalance or Crash?

While some headlines scream “crash,” the data suggests a different story. According to recent forecasts from the National Association of Realtors (NAR), home price growth has moderated to a manageable 2-3%, aligning closer to standard inflation rates. This indicates that while the market is “cooling” from its pandemic-era fever, it is stabilizing into what economists call a “balanced market.”

In early 2026, we are seeing a “thaw” in the lock-in effect. Homeowners who were clinging to 3% mortgage rates from 2021 are finally moving due to life-changing events—jobs, family growth, or retirement. This increase in supply is exactly what was needed to slow down the aggressive price bidding wars of previous years.

5 Key Signs Is the 2026 Housing Market Cooling?

To understand if the market in your specific area is losing heat, look for these five indicators that signal is the 2026 housing market cooling:

- Inventory Growth: Nationally, active listings are up approximately 10-15% compared to this time last year.

- Days on Market (DOM): Homes are sitting on the market for an average of 45-60 days, up from the 21-day average seen in 2023.

- Price Reductions: Nearly 25% of active listings now feature a price cut, a clear sign that sellers are adjusting expectations.

- Mortgage Rate Stabilization: With the 30-year fixed rate hovering around 6.2%, the rapid “shocks” to affordability have slowed.

- Buyer Sentiment: High-intent buyers are becoming more selective, no longer waiving inspections or appraisals.

Why Your Down Payment Matters More in a Cooling Market

In a hot “seller’s market,” your down payment was often just a ticket to get in the door. In a cooling 2026 housing market, your down payment is a strategic tool for risk management and cost reduction.

1. Lowering the “Interest Tax”

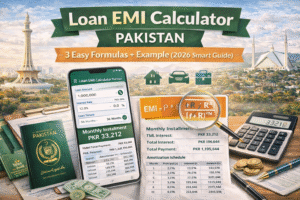

With rates around 6%, the total interest paid over 30 years is significant. A larger down payment reduces the principal balance immediately, saving you tens of thousands of dollars in interest. You can visualize this difference instantly by using our mortgage calculator to compare a 5% vs. a 20% down payment scenario.

2. Eliminating PMI (Private Mortgage Insurance)

In 2026, lenders have tightened their criteria. Avoiding PMI by hitting the 20% threshold can save the average buyer between $150 and $300 per month. In a cooling market where equity growth is slower, you don’t want to be “underwater” (owing more than the home is worth) because of a low-down-payment loan and a slight price dip.

3. Competitive Negotiating Power

Sellers in a cooling market are more risk-averse. They prefer a buyer with a 20% down payment over one with 3.5%, as it signals financial stability and a higher likelihood of the loan closing without issues. In 2026, a strong down payment can be the reason a seller accepts your “under-ask” offer.

The GEO Shift: Cooling Hotspots vs. Resilient Zones

The question “Is the 2026 housing market cooling?” depends heavily on GEO-location. Real estate in 2026 is highly bifurcated:

| Region Status | Typical Markets | Strategy for 2026 |

|---|---|---|

| Cooling Rapidly | Austin, TX; Phoenix, AZ; Florida Coast | Wait for further price adjustments; negotiate aggressively. |

| Steady Growth | Midwest (Chicago, Columbus); Northeast | Focus on long-term equity; high demand remains. |

| Price Stagnant | Pacific Northwest; California Tech Hubs | Look for “fixer-uppers” or motivated sellers. |

The Math: Using a Mortgage Calculator for 2026 Planning

Before you visit an open house, you must master your personal “affordability math.” Because is the 2026 housing market cooling, you have the luxury of time to plan. Use our finance calculator to assess your debt-to-income ratio (DTI) before applying for a pre-approval.

2026 Buying Pro-Tip: Don’t just look at the monthly payment. Look at the Amortization Schedule. In the first 5 years of a 6.2% loan, most of your payment goes to interest. A larger down payment changes this ratio in your favor from day one.

Frequently Asked Questions (AEO Optimized)

Is the 2026 housing market cooling for first-time buyers?

Yes, affordability is improving as income growth is finally outpacing home-price appreciation. While rates are higher than the 2020-2022 era, there is more inventory and less competition, making it a “Goldilocks” entry point for many.

Will home prices drop in 2026?

Most experts, including those from J.P. Morgan, expect prices to remain “flat” or rise modestly (0-2%) rather than drop significantly. The lack of supply still prevents a major price collapse.

How much down payment do I need in 2026?

While you can still buy with as little as 3-3.5% (FHA), a 10-20% down payment is recommended in 2026 to protect against minor market fluctuations and to secure the best possible interest rate.

Take the Next Step: Calculate Your Savings

Don’t guess your financial future. Use our suite of professional tools to see exactly how the 2026 market trends impact your wallet.

- Calculate your exact monthly cost: Mortgage Calculator

- Plan your long-term wealth: Compound Interest Calculator